A Rebalancing Guide: Part Two

MAIN TAKEAWAY

In PART ONE of this rebalancing series, we talked about why investors rebalance. In Part Two of this three-part mini series, we’re going to look at the optimal timing and scope of portfolio rebalancing.

KEY TALKING POINTS

Static calendar rebalancing is simple, but usually not optimal. If you’re going to use calendar-based rebalancing, do it 1x/year.

Pre-defined rebalance “tolerance” bands typically produce better outcomes than calendar-based rebalancing.

Frequent monitoring generally helps rebalancing results, but frequent trading does not.

There is disagreement in the research regarding whether or not rebalancing can enhance investor returns.

In general, wider tolerance rebalancing bands produce better returns than narrow ones.

THE RESEARCH

I tracked down all major white papers & research studies covering optimal portfolio rebalancing strategies I could find. I came across a few that required various member associations for access, so I left them out in favor of publicly available information.

Ultimately, 14 studies published between 1993 & 2024 were reviewed for this article*.

What follows are insights based on the research collectively suggest.

CALENDAR-BASED REBALANCING

This strategy involves picking a specific date(s) and executing portfolio trades to bring portfolio holdings back to their pre-determined targets.

Rebalancing frequencies can be annual, semi-annual, quarterly, monthly, or even weekly. This is a relatively simple portfolio management strategy that most investors can implement.

According to the research, when transaction & monitoring expenses are high, annual rebalancing is preferred. Additionally, annual rebalancing presents a stronger association with controlling for risk than enhancing returns.

Due to the age of some of these papers, I would push back on the cost component of the argument. At most retail brokerage firms, mutual funds generally cost around $25 per trade, U.S. stocks are free, and ETFs are free.

This means that investors can effectively manage a portfolio without transaction costs just by utilizing the correct mix of cost-efficient investments.

However, the tax cost, especially when short-term capital gains are present, is persistent over time and shouldn’t be ignored.

THRESHOLD-BASED TOLERANCE BANDS

This strategy differs from calendar-based rebalancing because it’s not static. Tolerance bands use pre-determined percentages as the basis for rebalancing events. It’s only after a tolerance exceeds a certain percentage of “drift” away from the target that a rebalance occurs.

Tolerance band percentages can either be defined as RELATIVE OR ABSOLUTE.

There is strong support for rebalancing using 20% - 25% “relative” tolerance bands, as well as 3% - 5% when using “absolute” percentages.

Here are a few examples.

For a holding with a 10% target within a portfolio that has been assigned a 20% relative tolerance band, it would need to appreciate to 12% or higher, or 8% or lower, before the position is rebalanced back to its original 10% target.

20% of 10% is 2%, which is why 12% and 8% are the thresholds in this case.

Thinking in terms of absolute percentages using the same holding’s 10% target, a 3% deviation away from the 10% target would mean the holding isn’t rebalanced until it grows to 13% of the portfolio or more, or decreases to 7% of the portfolio or less.

I know the math can give us headaches, but not all percentages are created equal based on how they’re defined.

There are a few other important findings of note.

First, there is general agreement in the research that wider bands are more advantageous over long periods of time than narrow bands.

In addition, the Hong/Dimensional paper (2021) & the Daryanani paper (2008) present the strongest case for threshold rebalancing bands compared to calendar-based rebalancing.

However, the research becomes somewhat mixed depending on how we define what is “advantageous”.

If tax efficiency (applies to taxable accounts only) and controlling for risk represent the advantage, then the research strongly supports threshold rebalancing over calendar-based rebalancing.

If the advantage is defined by enhanced returns & lower risk, then the evidence in favor of threshold-based rebalancing isn’t as strong, i.e., it’s mild and even debatable in some cases.

Last, threshold rebalancing shows a measurable advantage over calendar rebalancing in implementation efficiency & taxation, and sometimes in risk & return outcomes. But, the magnitude of the threshold-based rebalancing advantage is not large, which is why it’s debatable.

Bottom line for investors- if software can be employed for frequent monitoring, then establishing wide threshold rebalancing bands is superior to rigid (static) calendar-based rebalancing.

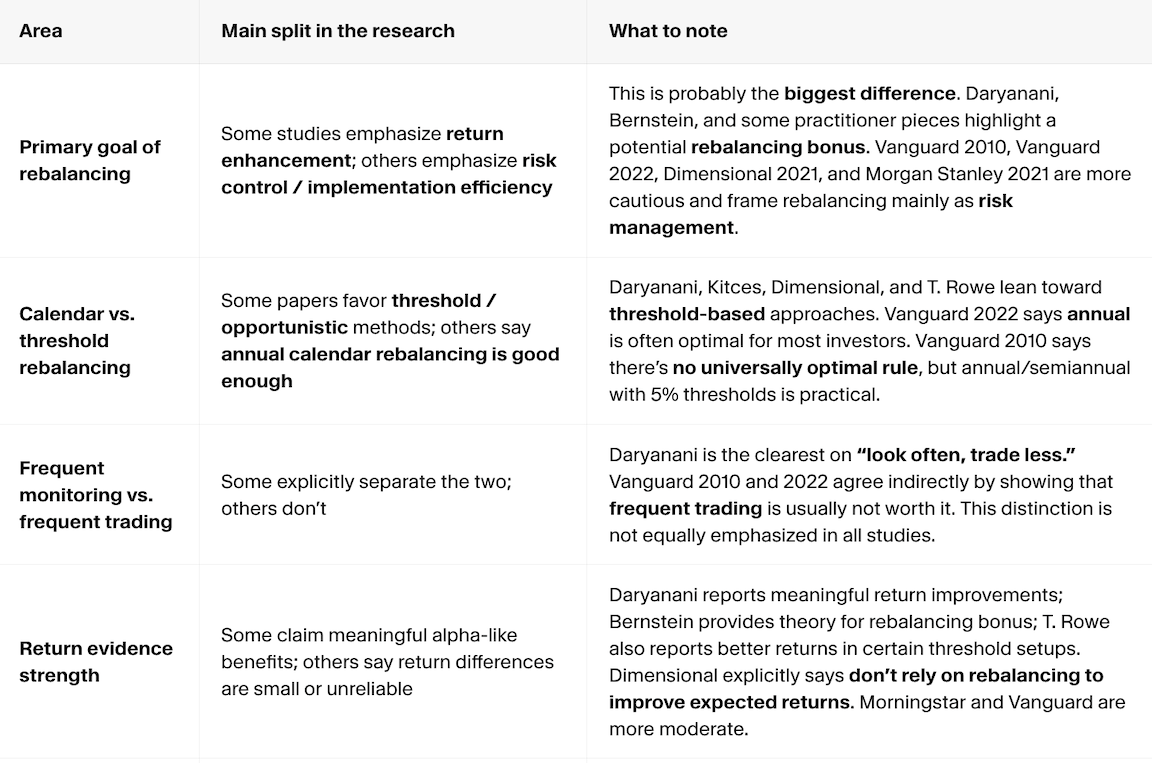

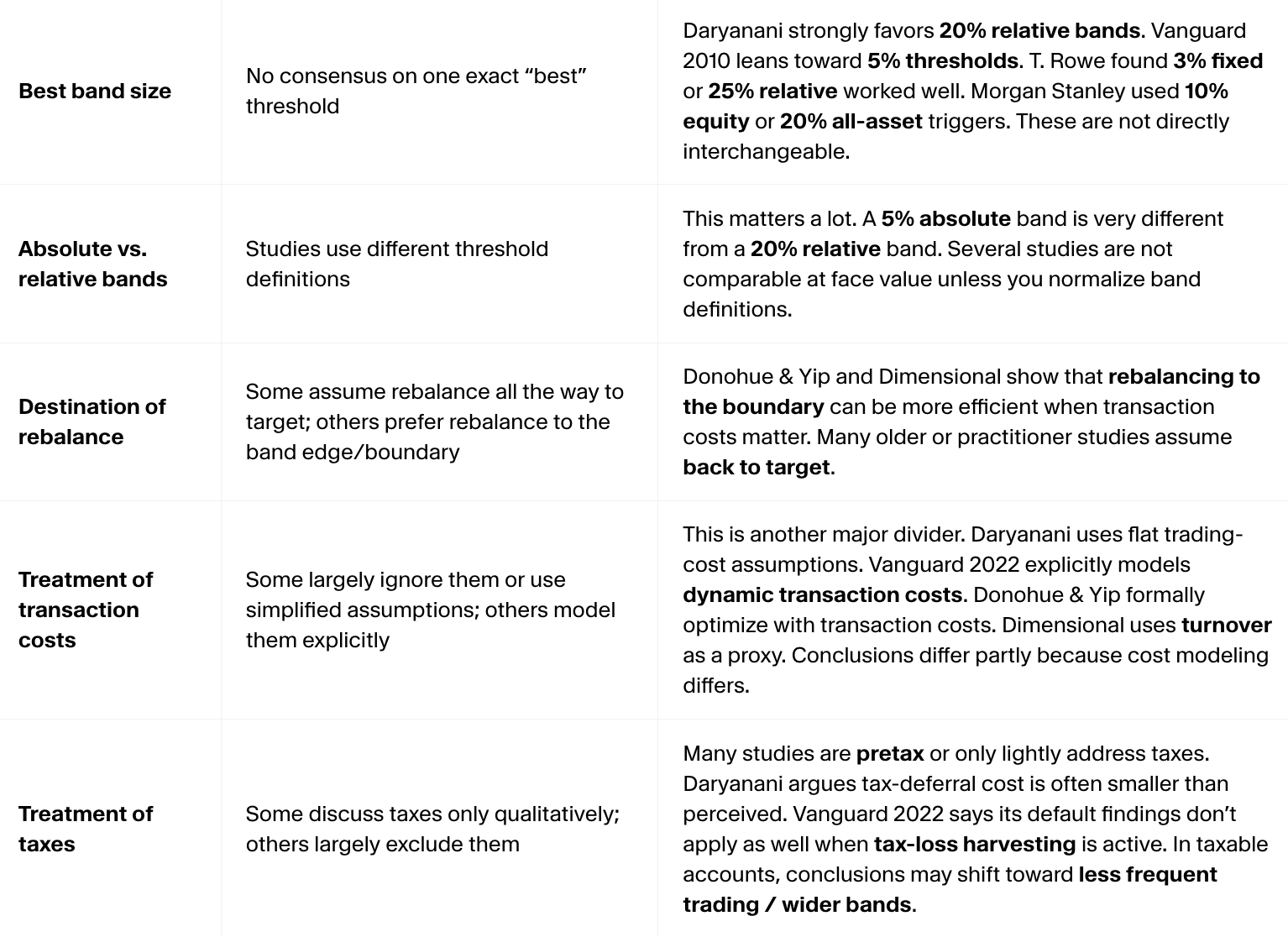

WHERE THE STUDIES DIVERGE

Different studies, measuring different asset classes, over different time periods, employing different rebalancing strategies, are likely going to come up with different results.

Not all studies are created equal, and that’s the case with the research surrounding portfolio rebalancing.

Some of the studies ask the question “How do we maximize return?”, while others ask “How do we keep risk aligned at the lowest cost?”. Some even ask, “How do we avoid worsening drawdowns during market crises?”

Below is a summary of all the major points where the studies diverge.

FINAL TAKEAWAY

Despite differences in how the studies were constructed, the broad consensus is that investors should implement a disciplined rebalancing policy, prefer thresholds to constant tinkering, avoid overtrading, choose a method that aligns with their operational capabilities, and stay tax sensitive when trading.

Here is a decision-making framework to help dial in your strategy, depending on your most important goal(s).

SIMPLICITY - Annual rebalancing with 5% absolute thresholds.

OPTIMIZATION - Frequent monitoring + pre-programmed tolerance bands using software.

TAX SENSITIVITY - Use wider bands, and rebalance using cash flows (sell-only trades for distributions & buy-only trades for contributions).

RISK - Use slightly narrower threshold-based tolerance bands.

If the research is overwhelming and you’re not sure what’s best, I don’t blame you. The tradeoffs in different rebalancing strategies for investors (all with unique circumstances) can be difficult to quantify.

Reach out!

If you’re currently a client at the firm and you’re not sure how we approach rebalancing, read PART ONE and ask for details as to how we’re managing your account(s) during your next scheduled review.

If you haven’t hired us yet, I doubt this is the post that convinces you we’re the right fit, but reach out anyway. I’ll help you understand what likely works best in your case, regardless of whether you ever hire us.

Stay tuned for Part 3 (I’ll work on this over the summer), where I’ll provide my own research findings as well as detail exactly how we program our software trading rules to produce optimal results across client portfolios.

Until then, thank you for reading, and have a wonderful day!

* Arnott & Lovell (1993) – “Rebalancing: Why? When? How Often?”

Donohue & Yip (2003) – “Optimal Portfolio Rebalancing with Transaction Costs”

Vanguard (2010) – “Best Practices for Portfolio Rebalancing”

Daryanani (2008) – “Opportunistic Rebalancing: A New Paradigm for Wealth Managers”

Hong / Dimensional (2021) – “Portfolio Rebalancing: Tradeoffs and Decisions”

Vanguard (2022) – “Rational Rebalancing: An Analytical Approach to Multiasset Portfolio Rebalancing Decisions and Insights”

Morningstar (2020) – “Why Rebalancing (Almost Always) Pays Off”

Morgan Stanley (2021) – “Resolving the Rebalancing Riddle for Institutional Clients”

T. Rowe Price (2024) – “What’s the Best Approach for Portfolio Rebalancing?”

Kitces (2016) - “Finding the Optimal Rebalancing Frequency - Time Horizons vs. Tolerance Bands”

Fisher / CFA Institute (2013) - “Does disciplined rebalancing improve outcomes?”

Granger, Harvey, Hemert / Duke University (2020) - “Strategic Rebalancing”

Berstein (1996) - “The Rebalancing Bonus”

Berstein (1996) - “When Doesn’t It Pay To Rebalance?”